Most diagnoses of venture capital's structural failure since 2012 have been directionally right about the mechanism and insufficiently precise about the load-bearing element. The element is liquidity.

The fee architecture only works because no liquidity event tests it. The narrative screen only survives because no liquidity rail price-discovers what the narrative is hiding. The fourteen-year holds, inflated marks, the DPI-versus-TVPI gap, and the missionary-versus-mercenary debate are all symptoms of one design flaw.

The venture instrument was built without programmed liquidity. Everything wrong with it is what you get when allocators with no exit path collide with managers paid for activity rather than outcomes. Fix the liquidity architecture, and the rest reorders itself.

Start in 2012.

In 2012, anyone could have been forgiven for thinking the venture capital industry was about to change. The Ewing Marion Kauffman Foundation, an institution built to fund entrepreneurship and a long-standing ally of the venture industry, had just published a report based on its own twenty years of experience as a limited partner in nearly one hundred venture funds. The title was a confession: We Have Met the Enemy and He Is Us.

The most significant misalignment, they wrote, occurs because LPs do not pay VCs to do what they say they will, which is generate returns that exceed the public market. They had the data to prove it. Of eighty-eight funds in their sample, sixty-nine (seventy-eight percent) failed to return enough to compensate for the fees, the carry, and the patience required to hold an illiquid asset for a decade. The best returns in their portfolio came from funds raised before 1996, and those funds averaged ninety-six million dollars in committed capital. As fund sizes grew, returns eroded and fee income increasingly accrued to managers at LPs' expense.

Three years after I wrote about the Kauffman report's 10-year anniversary, the evidence has piled up exactly as the past predicted.

Let's explore why the problem persisted, what the numbers look like now, and how Venture Capital 2.0 ships with native liquidity on board.

The model does not reward what it claims to reward

If you are like me and want to know the root cause of a problem, start with the mechanism. Everything you will want to understand follows from it. The standard venture fund charges two percent of committed assets per year plus twenty percent of profits. Kauffman put the consequence plainly:

under the two-and-twenty structure, many institutional investors pay general partners well to build funds, not to build companies.

Follow the money, and the model incentivizes one behavior above all others: the creation of bigger funds.

A general partner does not need a company to exit to get paid. The general partner needs to raise the next fund, and the next fund can be raised entirely on unrealized performance. Mark the book to the last priced round. There is no public bid to embarrass the mark. Report a TVPI line that looks like success and raise Fund IV on the strength of it, collecting a fresh two percent on a fresh pool of committed capital, before Fund II has returned a single dollar of cash to anyone.

DPI, the number that represents money actually returned to investors, is the number the general partner is structurally incentivized to defer. This is a liquidity failure dressed as an accounting one. Value on the books is not value in the bank.

Dan Gray, writing for Odin last month in The Magical Money Tree of Management Fees, has documented the same mechanism in real time with sharper edges than I gave it. His framing is that the linear scaling of management fees outpaces the sublinear scaling of returns from larger and later investments, so a growing share of every dollar of market expansion gets siphoned out as fees rather than earned as returns. He names a law for it, a knowing riff on Andreessen Horowitz, the firm whose AUM growth has come to symbolize the dynamic. Horowitz's Law: capital flows to wherever the fees are highest. I like that he puts a number on the drift.

The five firms that raised the most in 2005 each generated around one hundred fifty million dollars in subsequent fee income. For 2025, the comparable figure is closer to 1.6 billion.

That is the 2012 finding, compounded across fourteen more years of the same incentive doing the same thing.

The numbers now are worse than the numbers then

The picture has moved past underperformance and into something closer to mechanical impossibility.

AI now dominates the deployment side. In Q1 2026, the PitchBook-NVCA Venture Monitor reported $267 billion of U.S. venture deal value, with AI and machine learning representing 88.8 percent of it. The apparent exit recovery was just as concentrated: Q1 exit value reached $347 billion, but removing the five largest exits cuts that figure by 86.6 percent. In that quarter, the asset class was funding one category and clearing five names.

The distribution side has not recovered in anything like the same way. Recent North American vintages still show single-digit median IRRs and sub-1x median DPI, and the 2019 vintage has posted the weakest five-year DPI since 2006. Fewer than forty percent of 2019 and 2020 funds have returned any capital at all. Vintage fund performance has fallen to levels not seen since before the financial crisis.

Thin secondary markets have become the liquidity workaround rather than the exception. Private-market secondaries exceeded $225 billion in 2025, up more than 40 percent from the prior year. Liquidity is increasingly arriving through resale to the next bag holder rather than through companies actually reaching escape velocity.

The capital efficiency story makes the same point at the company level, and Gray reaches for the same example I used. Tesla raised roughly $200 million in private equity capital before going public, faced a genuine capital constraint, found efficiency under that constraint, and became a generational outcome. Rivian raised $10.5 billion in private capital before its IPO, never felt the same discipline, never developed the same efficiency, and has traded roughly eighty percent below its IPO price. As a vessel for allocation, Rivian absorbed roughly fifty times the capital and produced a fraction of the result. The fee income, of course, scaled with the capital absorbed, not with the outcome delivered.

This is what the screening process now selects for, and it is the opposite of what the industry tells itself it is selecting for. Not durability, not capital efficiency, not the outlier quality that actually drives venture returns. Gray reaches the screen and stops at filtering "for companies that are quick to revenue, easy to scale and legible to capital."

I will go one step further.

The screen does not need any of those traits to be real. It only needs the narrative shape that suggests them. Rivian was not easy to scale; it was easy to describe scaling. WeWork was not quick to revenue at the unit-economic level that matters; it was quick to a story about being quick to revenue, and the story remained legible to capital long after the operations beneath it stopped supporting the claim.

The screen rewards narrative shaped like inevitability, regardless of whether the operations beneath it are.

The survivors of that filter are often the companies public markets punish once they finally get a look at them. James Thomason traces this dynamic in Narratives pick the KPI, and the KPI picks the losers: the metrics that attract capital in emerging tech sectors systematically favor the companies least likely to dominate long-term. Gray's closing line is the right diagnosis: public markets want strong companies while private markets want big ones. The amendment I would offer is that private markets do not actually want big companies. They want big stories about big companies.

The defense of the structure does not survive its own evidence

The standard defense of two-and-twenty is the power law. Most funds fail. Most companies fail. But one Sequoia, one Benchmark, one early Google check returns the rest. The structure works in aggregate, the argument goes, because the asset class is shaped by outliers, and the outliers more than compensate for the failures.

A more sophisticated version of the same defense will argue that Kauffman's portfolio was a sub-median selection: top-quartile funds outside their sample did beat public markets, and the right response is better fund selection, not structural reform. Granted. But that is precisely the point.

When one of the most sophisticated institutional LPs in the world cannot reliably pick top-quartile funds, the asset class has stopped being an asset class and become a manager-selection problem dressed as one.

Even granting top-quartile outperformance, the structure now requires LPs to identify the top quartile ex ante, in an instrument where the median fund destroys value relative to public markets. And the screen that pushes companies to absorb more capital is making the right-tail outcomes worse, not better, by extending time-to-liquidity past the fund cycle for many companies. The burden of finding it only grows.

Look at what the screen now produces. The companies that survived capital constraint and went public early (Tesla on roughly $200 million pre-IPO, Amazon on roughly $16 million in venture capital, Apple on under $4M) might not clear the current screen. They would be pushed to consume more capital and stay private longer, because the structure rewards the GP for absorbing capital and rewards LPs only when the GP eventually exits. The power law was never a vindication of the structure. It was a vindication of the companies that escaped it. With escape velocities now extended past a decade, the structure has stopped producing the outliers that were supposed to justify it.

To be fair to fund managers, LPs are not innocent in this. Career risk pushes allocators toward the same names and the same vintages everyone else funds, because the wrong answer with consensus is forgivable and the right answer alone is not. Endowment and pension committees report against benchmarks built from the very funds that have generated the failures Kauffman described.

The result is a closed loop in which the GP raises bigger because the LP funds bigger because the benchmark allocates bigger. It has created a giant echo chamber, where breaking out requires a different instrument altogether.

Why fourteen years of correct critique changed nothing

If the Kauffman Foundation, one of the most credible LPs in the world, diagnosed this precisely in 2012, and if every honest observer since has confirmed it, why did nothing change?

Changing the model threatens short-term fund profitability and cannibalizes the fundraising machine whose entire purpose is to raise ever larger funds. The incumbents cannot reform themselves, because the thing that needs reforming is the thing that pays them. Inside the fund, fee income is durable revenue while carry is contingent. Allocating capital at scale builds a career, while shaping exits builds a war story. And funding consensus reliably raises the next fund, while finding outliers, by definition, does not. None of that is irrational from inside the fund. It is the rational response to the incentive, which is why exhortation has never worked and never will.

This is a classic Innovator's Dilemma.

Even visible LP pressure does not override the structure. Andreessen Horowitz announced more than $15 billion in new venture funds in January 2026, amid the asset class's weakest DPI vintages since the financial crisis. The structure wins because the structure is what allocates.

But there is a deeper reason the critiques failed, and it is the reason I want to press on now. Every critique stops at advice. The analysts and the data brokers can't say what needs to be said because most of them call VCs 'customers. I can only imagine the LPs in the market would rather just quietly slip out the back door and avoid the spotlights.

Kauffman told LPs to demand preferred returns, to negotiate better terms, and to conduct deeper diligence. Good advice, ignored for fourteen years. Gray tells LPs to pick the missionary over the mercenary, to reward conviction over consensus. Also good advice, and it will also be ignored, because it is selection advice offered inside the existing wrapper. You cannot select your way out of a structural problem. As long as the instrument pays general partners to raise rather than to return, a well-chosen missionary GP faces the same gravitational pull toward inflated interim marks the moment it is time to close the next fund.

The instrument is the problem. Telling people to use a broken instrument more wisely is a coping strategy, not a solution.

Venture Capital 2.0 Ships with Native Liquidity Built In

In Venture Capital 2.0, I argue that in the post-power-law era disciplined, repeatable venture-building, not lottery-ticket exits, will drive the asset class. This is true for several reasons that I explore, but none greater than the reconfiguration of liquidity management.

Safer (Simple Agreement for Future Equity with Repurchase) is central to the idea of liquidity reconfiguration. Safer is a hybrid structure that pays through distributions tied to company revenues on a defined cadence, not solely through an eventual equity sale.

Three changes do the work. Each targets a load-bearing element of the liquidity failure.

Removing the Terminal Liquidity Dependency

What if returns were not generated solely through an eventual equity sale? Revenue-aligned distributions begin when a portfolio company crosses defined operating thresholds, not when a board approves an exit a decade later. The instrument matches the timeline of company development rather than the timeline of fund cycles, which is the mismatch at the root of everything. Founders get patient capital. Allocators get a real cadence.

Fee architecture tied to Safer distributions, not to assets under management

A nominal annual operating fee covers the firm’s run cost (salaries, audit, fund admin, legal, regulatory), sized to operating reality rather than to capital under management. A $1B fund costs more to operate than a $100M fund, but not ten times as much. On top of that, the GP earns a percentage of every Safer distribution that flows to the LP. That is what the architecture realigns: not just incentives, but instinct.

When a partner’s compensation comes from the cash a portfolio company actually distributes, the partner spends time inside that company, not inside fundraising decks.

This is the structural reason I argue in the book that the future of venture belongs to builders: general partners whose returns are tied to operating outcomes, not to capital absorbed. Gray’s Horowitz’ Law, “capital flows to wherever the fees are highest,” stops being true the moment you change what the fee attaches to: fees can only be high where a portfolio company is producing real cash.

A future secondary market to replace the multi-year hold

A position held privately for fourteen years is a fee-generating vessel by default. The Safer breaks this by being a market-tradable instrument. Like an options contract, a Safer is standardized: defined cashflow rules, an explicit payoff structure, and a known underlying. Standardization is what makes any instrument tradable in a secondary market. It is the same property that allowed listed options to develop liquid exchanges in the first place, and it is the property that lets a Safer position potentially be priced and bid by counterparties who are not the original investor. The hold is no longer indefinite, and the price is no longer the GP’s to assert. An LP who wants out finds a buyer and sells, the way an option holder does. Underperforming positions face a real price, not a polite one. Overperforming positions return cash to LPs without forcing a company-killing IPO or acquisition timeline. The hold stops being a vessel for allocation and becomes a position you are expected to clear. A mark that gets tested by an actual bid stops being a marketing number.

These three are not independent fixes that can be picked off à la carte. They are three facets of the same move: building liquidity into the instrument where the original design left it out.

Together, they form a closed loop in which the GP is paid when the LP is paid, the mark is tested when a position clears, and the company’s actual operating reality is the only thing left to evaluate.

Patient capital, operational expertise, and time horizons that match how real companies are actually built are not disadvantages to be apologized for. Under Venture Capital 2.0 they are the entire edge.

Let's see how it works

James Thomason built a Monte Carlo simulation for Safer-architected funds, which I have made available free to Venture Capital 2.0 readers here. Using his simulation, I created a $25M fund, run with conservative assumptions and four parameterizations, producing three load-bearing results. The model assumes a twenty-five-company portfolio, fixed fund size, explicit revenue-share terms, capped exit outcomes, and net-of-fee LP returns.

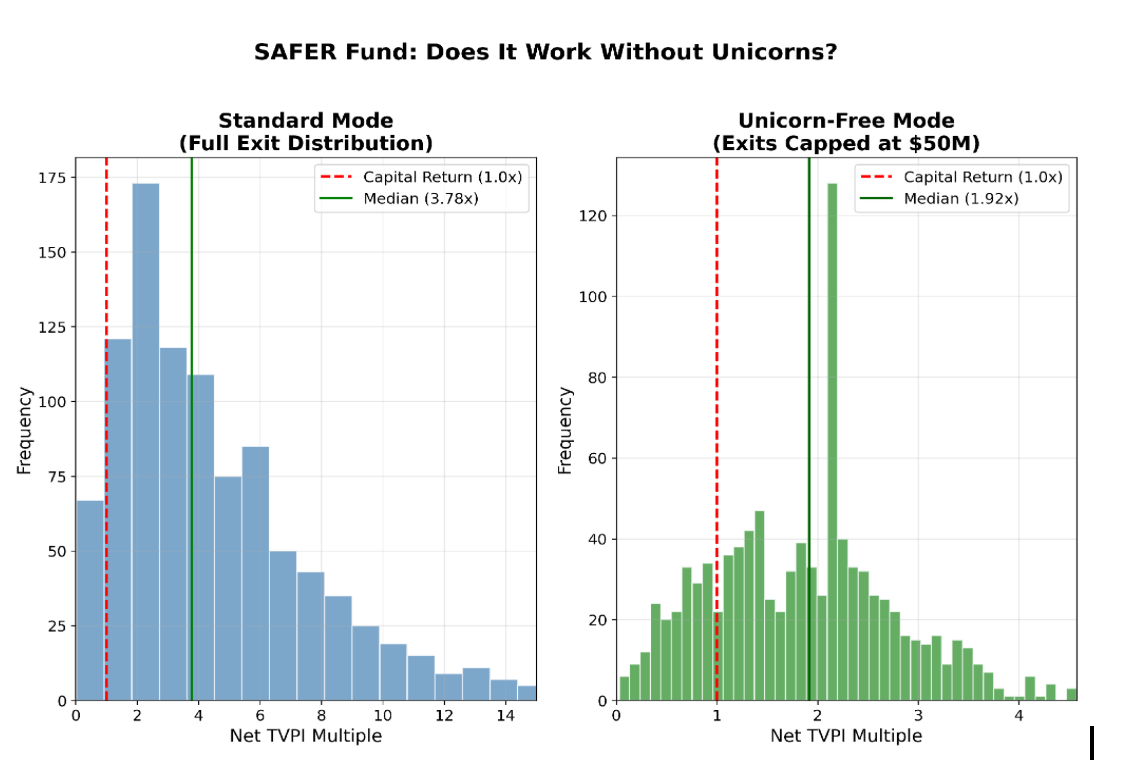

The architecture delivers without unicorns. This is the empirical claim James makes the technical case for in Venture Capital Without Unicorns. In a standard VC parameterization, 82.5 percent of simulation iterations are carried by an exit above $100M. Cap every exit at $50 million across the entire portfolio and standard VC collapses. The Safer architecture, run the same way, still returns a median 1.92x capital and 11.8 percent net IRR with no exit anywhere in the fund above $50 million. The revenue share is the floor. Unicorns add 1.87x on top of it. The asset class stops requiring lottery tickets.

Figure 1. TVPI distribution, standard parameterization vs. exits capped at $50M. The Safer architecture's revenue-share floor sustains a 1.92x median even when no portfolio exit clears $50M.

DPI cadence is real, not terminal. The median Safer fund returns 1x capital in 6.2 years and reaches a median net TVPI above 3.7x. 85.8 percent of simulated funds clear 1x DPI within the fund life. Cash moves on a cadence the LP can plan around rather than a terminal event a decade out.

Return composition shifts with the parameterization. In a Standard-VC setup, 86 percent of returns come from equity exits, 6 percent from revenue share, and the balance from other modeled proceeds, the legacy power-law shape. Reparameterize the same architecture for traction-selected companies ($350K+ ARR) and revenue share rises to 15 percent of returns; tune the terms toward yield and revenue share rises to 26 percent; push to $1M+ ARR companies with aggressive yield terms and revenue share becomes 52 percent of returns. The fund's economics stop being lottery-dependent and become yield-driven. The right tail still exists, but it is now upside instead of survival.

The full Monte Carlo output, including the four-scenario comparison, the unicorn-free stress test in detail, and the methodology, is in complimentary research download: Modeling Venture Capital 2.0.

Why now

Three things have changed since I wrote the 2023 piece, and all three are liquidity events. The asset class is being repriced around the missing element.

First, LP DPI pressure has become the dominant emotional state in the asset class. McKinsey's 2025 LP survey found that 2.5 times as many LPs now rank DPI as a "most critical" performance metric compared with three years prior. DPI rose to 21 percent of respondents naming it most critical, up from 8 percent three years earlier. In effect, CIOs are no longer asking whether returns will arrive; they are asking when, and the question is being asked in writing.

Second, GP fatigue has set in. The firms that raised mega-funds since 2016 are sitting on books they cannot mark up further and cannot mark down without consequence, and the next fund is harder to raise than the last in a way it has not been in twenty years. The Q1 2026 PitchBook-NVCA Venture Monitor reports that 90.9 percent of capital raised in Q1 2026 went to established managers, the highest share on record, and 73.1 percent of the quarter's commitments went to just five firms. First-time fund formation collapsed from 461 funds in 2021 to 106 in 2025. PitchBook's own framing: the fundraising market is "practically closed to most emerging managers."

Third, the secondary market is mere window dressing. Secondary volume crossed $210 billion in 2025, but look closely. The dominant form is GP-led continuation vehicles: discounted asset rollovers that let general partners extend fee streams on stranded portfolios while frustrated LPs take haircuts to get out. The CV racket is evidence that the liquidity problem has gone systemic, not infrastructure that fixes it.

Exploiting the Innovator's Dilemma

History rhymes here. Every prior structural calamity in capital markets produced its own emergent platform. The 2008 financial crisis gave us Stripe and the rise of fintech. The dot-com bust produced Google's ascendancy and the rebuilding of internet commerce on more durable economics. The Great Depression gave us modern securities regulation and the rise of mutual funds. The pattern is consistent: when the existing infrastructure shows it cannot handle current conditions, alternative platforms gain share. The incumbents cannot match them on equal terms because they cannot abandon the business that funds their existence.

Christensen explained how a new entrant takes a foothold at the bottom of the market, among customers the incumbents either cannot profitably serve or have stopped noticing. The new offering is "good enough" for that segment but cannot compete head-to-head at the top end. As its capability improves, it moves upmarket. The incumbents, structurally committed to the customers and economics they already have, cannot respond without breaking their own business. Eventually, the new entrant takes the profitable segments too. Disk drives, steel, retail, mobile telephony, and online banking: each was disrupted on the same trajectory.

This is playing out in venture finance now.

The architecture that replaces 2/20 will not arrive announced and authorized. It will accrete out of the customers the legacy fund cannot profitably serve. Family offices priced out of top-tier funds will fund the alternatives. Capital-efficient founders will take the better terms. LPs frustrated with continuation-vehicle haircuts will move their next allocation to a vehicle that distributes on cash. None of this requires the industry to agree. It only requires the math to keep being the math.

Download the full Monte Carlo simulation output and analysis (email registration required)

Upgrade to Premium and joing the Venture Capital 2.0 movement. John will send you complimentary digital copies of his books!