Spoiler Alert: It's you and me.

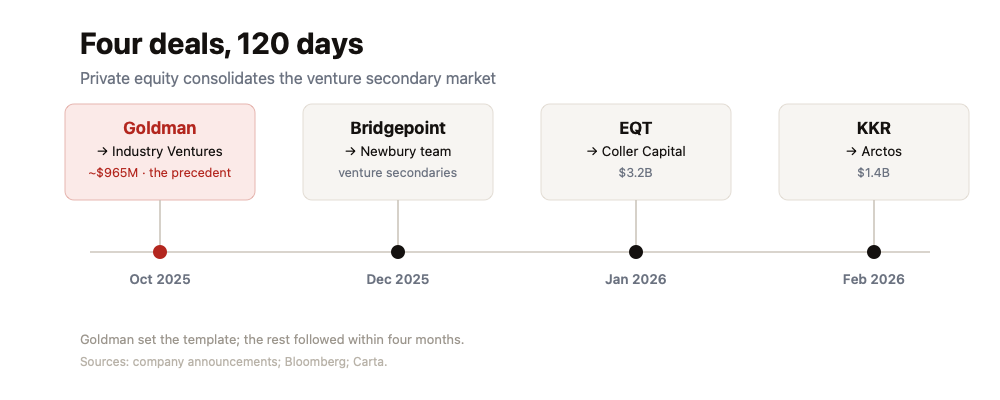

Last October, Goldman Sachs bought Industry Ventures, a deal that mattered more than its price tag let on. There was blood on the streets, and Goldman had just bought the mop company. The largest balance-sheet institution in finance had decided that the most valuable position in private markets was no longer the asset, but the desk that lets you out of it.

In the weeks bracketing Goldman's January 2026 close, the three other largest names in private capital made the same move. Bridgepoint took the Newbury Partners secondaries team in December. EQT agreed to combine with the $50 billion specialist Coller Capital for $3.2 billion in January. KKR agreed to acquire Arctos in a deal initially valued at $1.4 billion in February. Four of the most sophisticated allocators on earth, inside a hundred and twenty days, all chose to own the secondary market rather than merely trade in it.

It kinda makes you wonder, what gives?

Well, they bought a fee machine. Fine. That's not unusual. But that is only the headline. The story that matters is who buys what these desks sell.

What a secondaries firm actually sells

A secondaries firm sells one thing: liquidity to investors who cannot get it from the funds they are already in.

When a limited partner needs cash out of a fund that isn't returning capital, the secondaries desk buys the position at a discount, and the LP gets liquidity it could not otherwise generate. When a general partner cannot sell or float a portfolio company, and will not mark it down or hand it back, the desk helps roll it into a continuation vehicle, moving the asset from one fund the GP controls into another fund the GP controls, with fresh money paying out the original investors. Either way the product is the same, synthetic liquidity for capital the underlying engine failed to free.

That is the lens to bring to the headline number.

Global secondaries volume hit a record $226 billion in 2025, up 41% on the year, by Evercore's count as reported by Bloomberg. The figure measures distress; the amount of money that needed a manufactured way out because the natural ways out weren't there. The composition makes the point:

LP-led volume rose 34% to $120 billion, while GP-led volume, where the manager engineers the exit for assets it already holds, rose 51% to $106 billion.

The faster-growing half is the more synthetic one. A record in secondaries volume is a record in the demand for escape, and the market grew because the thing it stands in for, real exits, kept not arriving.

The DPI backdrop nobody wants on the cover slide

To see why escape became a growth business, look at what funds have actually returned to investors in cash rather than in marks. Carta's first-quarter 2026 performance data tells the story the marketing decks leave out.

Among 2017 and 2018 vintage funds, now eight and nine years into their lives and well past the point where distributions should be flowing, fewer than one in five has returned even the capital it called.

For the 2019 and 2020 vintages, the median fund has distributed close to nothing. Total value, which includes unrealized marks, looks healthier, but a mark is an opinion and a distribution is a bank statement, and the gap between the two is the whole problem.

This is the pressure that built the secondaries market. An asset class that promised liquidity through public offerings and acquisitions has spent the better part of a decade failing to produce it at the scale the model assumes. Limited partners need distributions to meet their own obligations and to fund their next commitments, and when the exits don't come the pressure has to go somewhere. It went into a product:

liquidity, manufactured and sold back to the people who were promised it for free.

The secondaries boom is the relief valve, and in 2026 the valve got big time owners.

Buying the counterparty

Coller, Newbury, Industry Ventures, and Arctos are the desks other managers call when a fund needs to manufacture an exit, buying LP stakes at a discount and leading the continuation vehicles that move stranded assets into fresh wrappers.

That is what EQT, KKR, Bridgepoint, and Goldman acquired.

Goldman is the clearest case of why this makes sense for a buyer. It carries no carry-and-pray venture incentive; it is a fee-and-spread institution with a balance sheet built to own infrastructure. Buying Industry Ventures was never a bet on picking winners. It was a toll booth on other people's need for liquidity, bought just as the traffic was about to explode. EQT, KKR, and Bridgepoint are competitors refusing to cede the booth. Each looked at a decade of thin distributions, concluded that the liquidity function had become worth more than the origination function, and bought the function.

But here's the thing.

Owning that machine changes what a secondary transaction is. The firm that owns the desk now stands on both sides of the same asset. It buys the exiting LP's position, or sponsors and prices the continuation vehicle, as principal, and then places the exposure with capital it also controls via its evergreen funds, its wealth feeders, its insurance balance sheet, etc. It takes the discount going in and sells near par going out, and the spread between those two prices is the business. The buyer, the appraiser, and the reseller become the same house, and the customer at the far end of the chain is the one least able to argue with the number.

In a working market the secondary buyer is the adversary across the table, motivated to bid low because it keeps the discount, and that tension is where the price comes from. Buy the buyer, seat it beside the capital that funds it and the channel that resells it, and the discount becomes an internal transfer between two desks of one firm, booked at whatever number suits the house!

Who's actually on the other side of the trade

Here is what I've been curious about.

If LPs are selling trapped positions and GPs are rolling assets into continuation vehicles, someone is writing the checks, and the identity of that someone has quietly changed.

The visible buyers are dedicated secondaries firms, and the industry is bigger and more concentrated than most people assume.

Ardian just closed the largest secondaries fund in history at $30 billion. Lexington Partners and Blackstone Strategic Partners, whose platform runs around $100 billion, each raised flagships north of $20 billion. The ten largest buyers accounted for more than half of all deployment in 2025.

These are the specialists whose whole business is to buy other investors' trapped stakes and sponsor the vehicles that recycle them.

Ok, seems legit, right?

Well, the more important shift is in the money behind those firms. The marginal new dollar buying LP stakes arrives through three overlapping channels.

Evergreen and semi-liquid funds, now around a quarter of secondaries buyers and the fastest-growing source of demand, are also the least price-sensitive money in the market. In the first half of 2025 they paid an average of 91 cents on the dollar of net asset value, more than four points above the rest of the market, outbidding the buyers who used to insist on a discount of twenty to forty percent.

Private wealth and retail capital, much of it flowing through those same evergreen wrappers, made up about a third of the money raised for secondary strategies in 2024, routed through the '40 Act funds, ELTIFs, and LTAFs built to put private markets in front of individuals.

And insurance and annuity balance sheets supply the permanent capital underneath it all, which is part of why EQT wanted Coller's insurance book and part of why the largest managers have spent five years assembling insurance-funded credit machines.

Goldman's own rationale for their deal included distribution leverage through its private wealth channels hungry for discounted tech exposure. This is where that channel leads. The wealth client, the retail account, and the retirement saver are the buyer, and they are buying close to the marked price rather than the cleared one.

It's you and it's me. It's our capital.

The desk was only half of what these firms bought; the other half is the pipe that carries a hard-to-price asset off a sophisticated seller's books and onto a less sophisticated buyer's. The mop company gets paid by the gallon, and the bucket is handed to whoever stands at the end of the line.

One position, end to end

Let's follow the money in a hypothetical example transaction.

Meridian Fund III is a 2014-vintage, $500 million venture fund in its twelfth year, past its contractual life and on a second extension. It has returned seventy cents on the dollar in cash. Almost all of the value that remains sits in one position, a late-stage company bought for $12 million in 2016 and carried today at $180 million.

There is no public offering on the horizon and no acquirer anywhere near $180 million. The GP cannot sell it, cannot hand it back without admitting the mark was fiction, and cannot afford to write it down while raising Fund VI. The asset is stuck, and so are the LPs behind it, a couple of endowments, a public pension, and a few family offices, all long past the date they expected their money.

So the GP rolls the position into a new vehicle, Meridian Continuation Fund I, with a venture-secondaries desk like Industry Ventures leading and pricing the transaction. An independent fairness opinion blesses a 25 percent discount to the GP's own $180 million mark, which sets the transfer at $135 million. The number does double duty:

it is a discount to the last mark and still eleven times the original cost, so it reads as prudent and triumphant at once. And it is measured against a mark the GP set, with no outside transaction confirming either figure.

The legacy LPs are offered a choice that isn't much of one. Roll into the new vehicle, or take cash. Across the market, eight to nine out of ten take the cash because they are exhausted and need distributions. They sell at the $135 million valuation, accept the haircut to the paper mark, and are relieved to be out.

Which leaves the only question that matters here: where does the cash to pay them come from? Fresh capital raised into the continuation fund, perhaps $150 million once fees and reserves are counted, and that capital increasingly arrives through the buyer's own private-wealth distribution channel and the evergreen and insurance vehicles feeding the bid. They come in at around 91 cents on the new $135 million valuation, near par to a mark the same house produced. The discount the GP extended to the departing institutions is the markup the arriving retail and insurance money pays.

If you've followed along so far, you might have noticed that one firm sits at every step.

Yep.

The Industry Ventures desk leads and prices the vehicle, Goldman's wealth and insurance channels place the stakes, and Goldman's balance sheet can lend against the asset on top.

The house collects a structuring fee, a placement margin of two or three points, a management fee of about 1.75 percent on $150 million for eight to ten years, and a spread on any loan against the position, perhaps $25 to $30 million over the life of the vehicle, owed whatever the asset finally does. Goldman is the mop company, there is blood on the streets, and they are being paid handsomely by the gallon.

Then time passes.

If the company eventually clears above $135 million, everyone looks vindicated. If the markdown the GP deferred finally lands and it sells for $80 million, the roughly $55 million loss falls on the evergreen, insurance, and retail buyers who came in last, not on the endowment that cashed out near the top. The sophisticated early money used the continuation vehicle to move the downside onto the least sophisticated holder, and the house was paid at every step of the move. Consolidation puts all of it under a single roof, and the 2026 deals are the industry buying the right to run the sequence at scale.

The price-discovery problem

When the same platform structures the exit, prices it, and owns the capital that buys it, three reference points that used to discipline the mark quietly disappear.

The independent bid is the first to go. A continuation-vehicle discount used to be negotiated against an outside buyer; when the buyer is an affiliate, the discount is set by the same people who profit from where it lands, and there is no arm's-length number left to check it against.

The exit stops being a test. A sale to a third party proves the asset was worth something to someone with no reason to flatter it. A transfer into an affiliated vehicle proves only that the firm was willing to move the asset from one of its hands to the other; the realization no longer validates the valuation, it just resets the clock.

And the conflict turns structural rather than occasional. Regulators have circled GP-led secondaries for this reason, and the SEC's private-fund rules already pushed toward fairness opinions and disclosure on adviser-led deals. Consolidation makes the conflict permanent and industrial instead of deal-by-deal. The wall between the firm that owns the asset and the firm that prices your way out of it is now an org chart, not a market.

Believe it or not, none of this is illegal, and a continuation vehicle can be a perfectly good outcome for an LP that needs cash. The harder problem is that the mechanism which used to tell you whether the outcome was fair is the very mechanism being absorbed.

How a Genuine Secondary Market Would Function

It's obvious to outsiders the venture capital industry is conceding the exit was never as reliable as the model needed it to be. The exit was supposed to be the proof, the moment a paper mark turned into real money and justified everything upstream. The secondary is the admission that the proof can be deferred for as long as another unwitting mark will keep buying the position, and consolidation is how that deferral gets industrialized and owned.

Do you like my work? Please consider upgrading to a paid subscription! You'll get access to private research, book copies and agentic tool kits... As always, I am grateful for your support. :)

As much as I shake my head at what smells like a Secondary market grift, trapped capital is real, the liquidity need is real, and a well-run secondaries platform can serve it. And to be clear, not every retread is a lemon. The best companies can get rolled because they're too good to dump into a weak exit market, and the buyer's bet that a brand-name asset will eventually IPO higher can legitimate, if optimistic.

However, if a single platform is going to own both sides of an exit, the price of admission must structural transparency.

The valuation has to be set or verified by someone with no stake in the outcome, a real fairness opinion with its method disclosed rather than a courtesy stamp. There has to be a documented wall between the people holding the asset and the people pricing the transfer, and the LP's right to take cash at the independent mark instead of rolling on the affiliate's terms. And every affiliated transaction has to be disclosed in full, its discount, its outside comparables, and the fees the firm collects on both sides.

None of that is exotic or radical. It is simply what a functional and efficient market would do.

The fine print right now is anyone buying secondaries through an evergreen or private-wealth product, rather than selling into one, should understand they are now the counterparty on this trade. The discipline that used to live in the discount-seeking buyer is discipline they have to supply themselves.

At the end of the day, what these firms are doing is rational and, on its own terms, well built. You kinda have to tip your cap to the evil genius of it all. They saw that in a market starved of exits the durable franchise is not picking the next winner but owning the door everyone eventually has to walk through. The question I think we should force is whether a market can find a fair price when the buyer, the appraiser, and the dealer reselling the asset have all moved into the same building, and the investor left holding the risk was never in the room.

How to keep score of the game

The further the marginal dollar shifts from informed institutions toward retail, wealth, and insurance money paying near par, the closer the risk sits to the public and the more degraded price discovery has become. That migration can be measured - I call it the Marginal Buyer Index:

the share of trapped assets absorbed by the least price-sensitive capital, the compression of discounts toward net asset value, the continuation-vehicle share of volume, and the distance between paper marks and realized cash.

When the public becomes unwitting buyer of last resort, the number goes up. More on that soon.

Sign up to get the latest from Venture Capital 2.0! It's free.

Sources:

Evercore secondaries volume via Bloomberg and Pensions & Investments;

Goldman Sachs, Industry Ventures announcement and completion;

Carta VC Fund Performance Q1 2026 and secondaries-market consolidation;

buy-side composition via PitchBook (private wealth pricing pressure), PitchBook (capitalization conundrum), S&P Global (secondaries fundraising), and Apollo (secondaries as core allocation).